Life Insurance for Retirement Planning

A key ingredient in a tax-smart strategy

Who Should Consider Life Insurance Retirement Planning?

-

High-income earners concerned about hitting qualified plan contribution limits

-

Entrepreneurs seeking to make up missing contributions to their own retirement income plan

-

Businesses looking to reward and retain key executives by providing supplementary retirement benefits

Prepare Your Clients for Retirement with a Healthy Mix of Retirement Assets

Your clients may plan to meet their retirement income needs with a mix of assets held both in and outside of retirement plans. Are they overlooking other sources of potentially tax-free1 supplemental retirement income such as cash value life insurance?

Strategy In Action

See how clients might benefit from a life insurance retirement plan.

1. Meet Isabela García Castillo

Isabela is a 50-year-old married mother with 2 teenagers. She is a successful real estate entrepreneur who plans to retire at age 67.

2. Facing Retirement Income Shortfall

She is maxing out contributions to her individual retirement account (IRA) and is concerned she won’t be able to save enough for retirement. She schedules a meeting with her financial professional7 to review her options.

3. Creating a Plan

They discuss her current portfolio and potential retirement income shortfall. Because she is generally healthy, more than 10 years from retirement, has available cash flow, and needs more life insurance, he recommends a cash value life insurance policy.

4. While She Works

She completes underwriting and then qualifies for coverage. Her policy provides life insurance protection while she works and pays premiums, and the policy accumulates cash value tax deferred.

5. In Retirement

After retirement, Isabela supplements her retirement income with income tax-free1 distributions from her policy’s available cash value. At her death, her beneficiaries receive an income tax-free death benefit.6

Connect with your Pacific Life representative to find tax efficient

strategies for your clients!

Contact us today for a demonstration, to request a personalized illustration, or for help submitting a case.

Explore Popular Resources

The primary purpose of life insurance is to provide death benefit protection in the event of the insured’s death.

Life insurance is subject to underwriting and approval of the application and will incur monthly policy charges. In general, additional premium is required to continue coverage of the policy. Policy may lapse if premium is insufficient to continue.

Pacific Life, its affiliates, their distributors, and respective representatives do not provide tax, accounting, or legal advice. Any taxpayer should seek advice based on the taxpayer’s particular circumstances from an independent tax advisor or attorney.

Insurance products and their guarantees, including optional benefits and any crediting rates, are backed by the financial strength and claims-paying ability of the issuing insurance company. Look to the strength of the insurance company with regard to such guarantees because these guarantees are not backed by hte independent broker/dealers, insurance agencies, or their affiliates from which products are purchased. Neither these entities nor their representatives make any representation or assurance regrading the claims-paying ability of the issuing company.

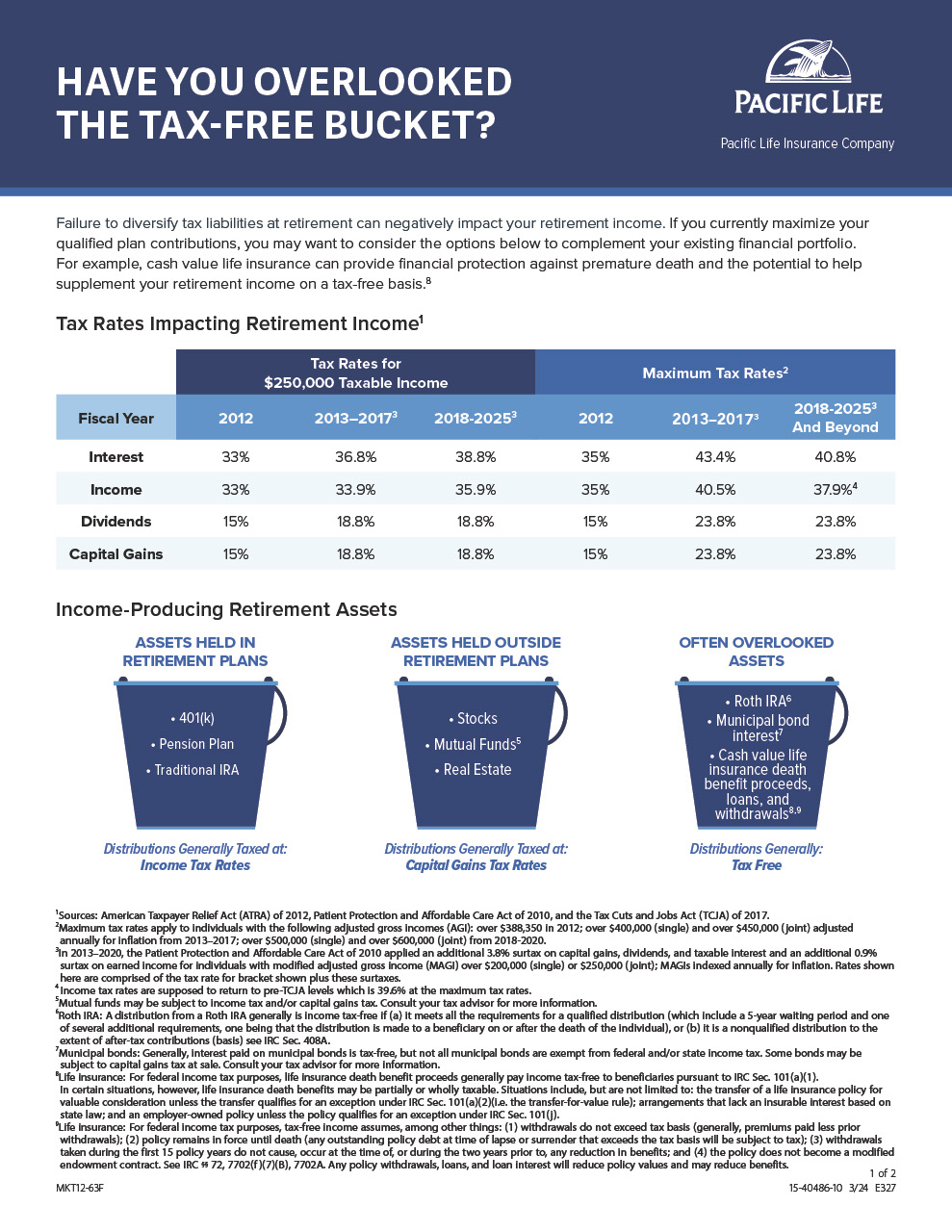

1For federal income tax purposes, tax-free income assumes, among other things: (1) withdrawals do not exceed tax basis (generally, premiums paid less prior withdrawals); (2) policy remains in force until death (any outstanding policy debt at time of lapse or surrender that exceeds the tax basis will be subject to tax); (3) withdrawals taken during the first 15 policy years do not cause, occur at the time of, or during the two years prior to, any reduction in benefits; and (4) the policy does not become a modified endowment contract. See IRC Sec. 72, 7702(f)(7)(B), 7702A. Any policy withdrawals, loans, and loan interest will reduce policy values and may reduce benefits.

2Mutual funds may be subject to income tax and/or capital gains tax. Consult your tax advisor for more information.

3Traditional IRA: If you are covered by a qualified retirement plan at work, traditional IRA contributions are fully deductible only if your adjusted gross income falls with the following 2024 limits: single up to $77,000; married filing jointly up to $123,000. Aug. 2024. Source: 2024 IRA contribution and deduction limits effect of modified AGI on deductible contributions if you are covered by a retirement plan at work

4Municipal bond: Generally, interest paid on municipal bonds is tax-free, but not all municipal bonds are exempt from federal and/or state income tax. Some bonds may be subject to capital gains tax at sale. Clients should consult their tax advisors for more information.

5Source: Tax Cuts and Jobs Act 2017.

6For federal income tax purposes, life insurance death benefits generally pay income tax-free to beneficiaries pursuant to IRC Sec. 101(a)(1). In certain situations, however, life insurance death benefits may be partially or wholly taxable. Situations include, but are not limited to: the transfer of a life insurance policy for valuable consideration unless the transfer qualifies for an exception under IRC Sec. 101(a)(2)(i.e. the transfer-for-value rule); arrangements that lack an insurable interest based on state law; and an employer-owned policy unless the policy qualifies for an exception under IRC Sec. 101(j).

7In order to sell life insurance, a financial professional must be a properly licensed and contracted life insurance producer.