Passing wealth to the next generation using life insurance

Wealth Transfer

Client Profile

Prepare Your Clients

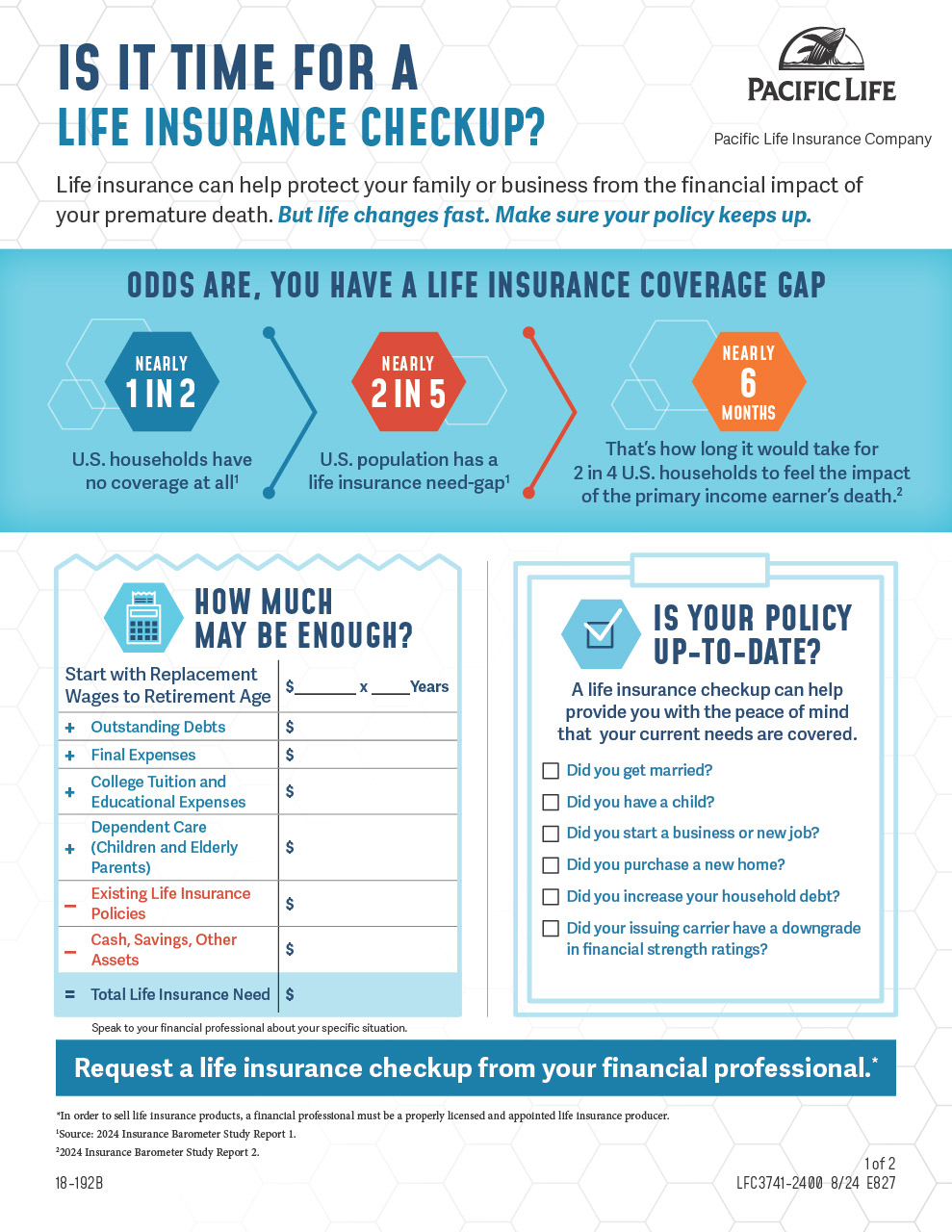

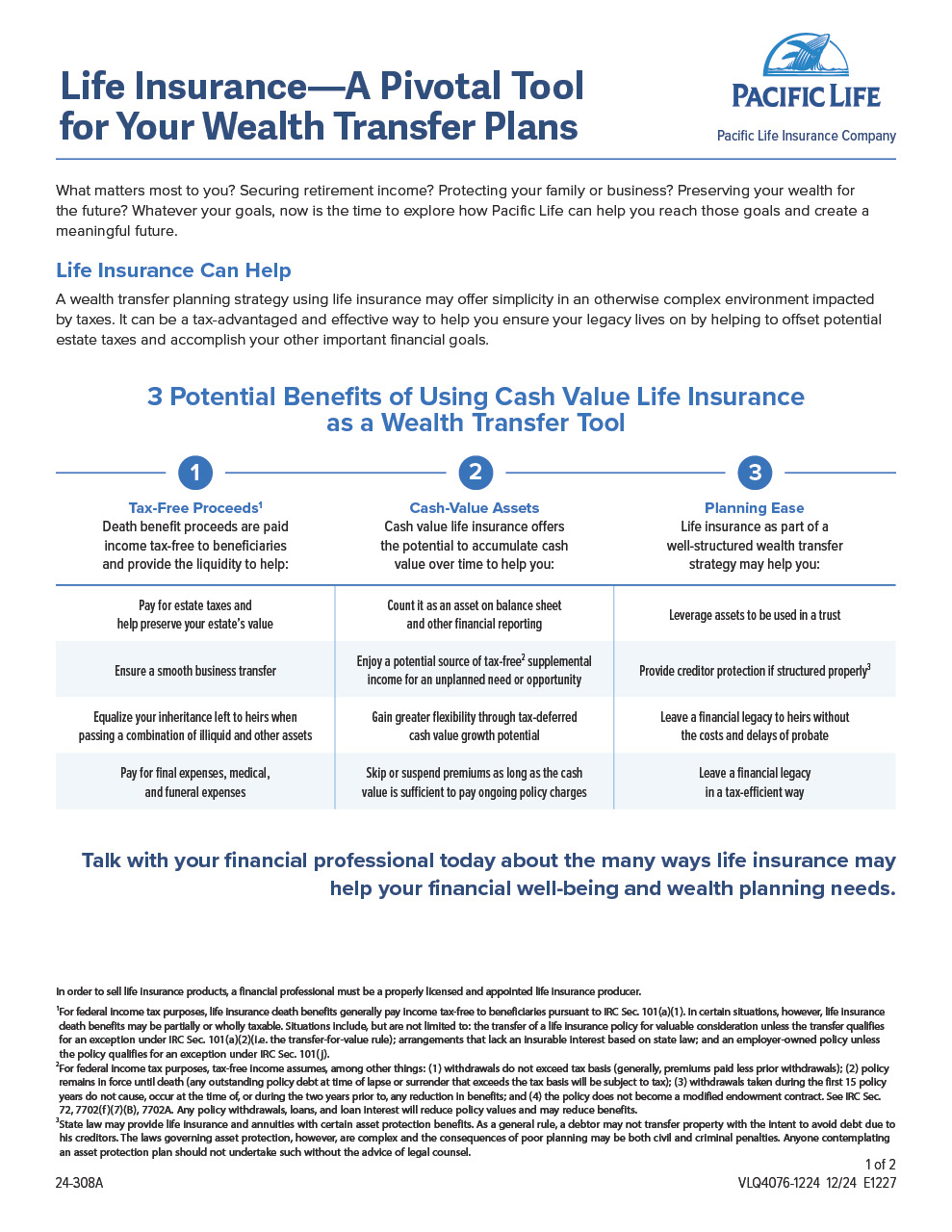

Only 34% of Americans have an estate plan in place.2 Plus, estate plans take time. That's why we've put together resources to help you plan ahead and help your clients efficiently transfer their wealth. Using life insurance as a wealth transfer tool provides three main benefits.

Learn more: Why Life Insurance as a Transfer Tool

Strategy In Action

Key steps to help develop effective wealth transfer strategies with your clients today.

1. Identify Wealth Transfer, Estate, and Succession Planning Needs

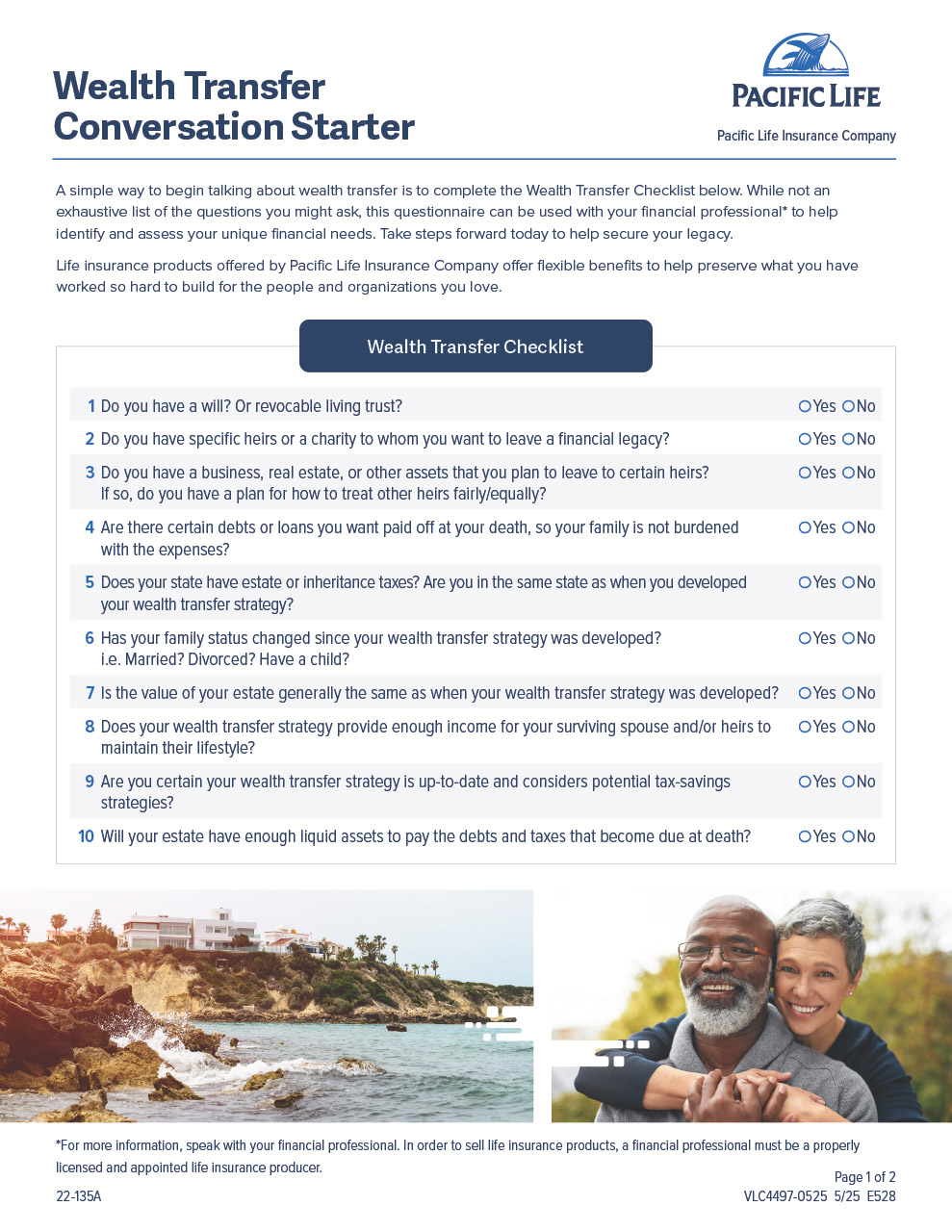

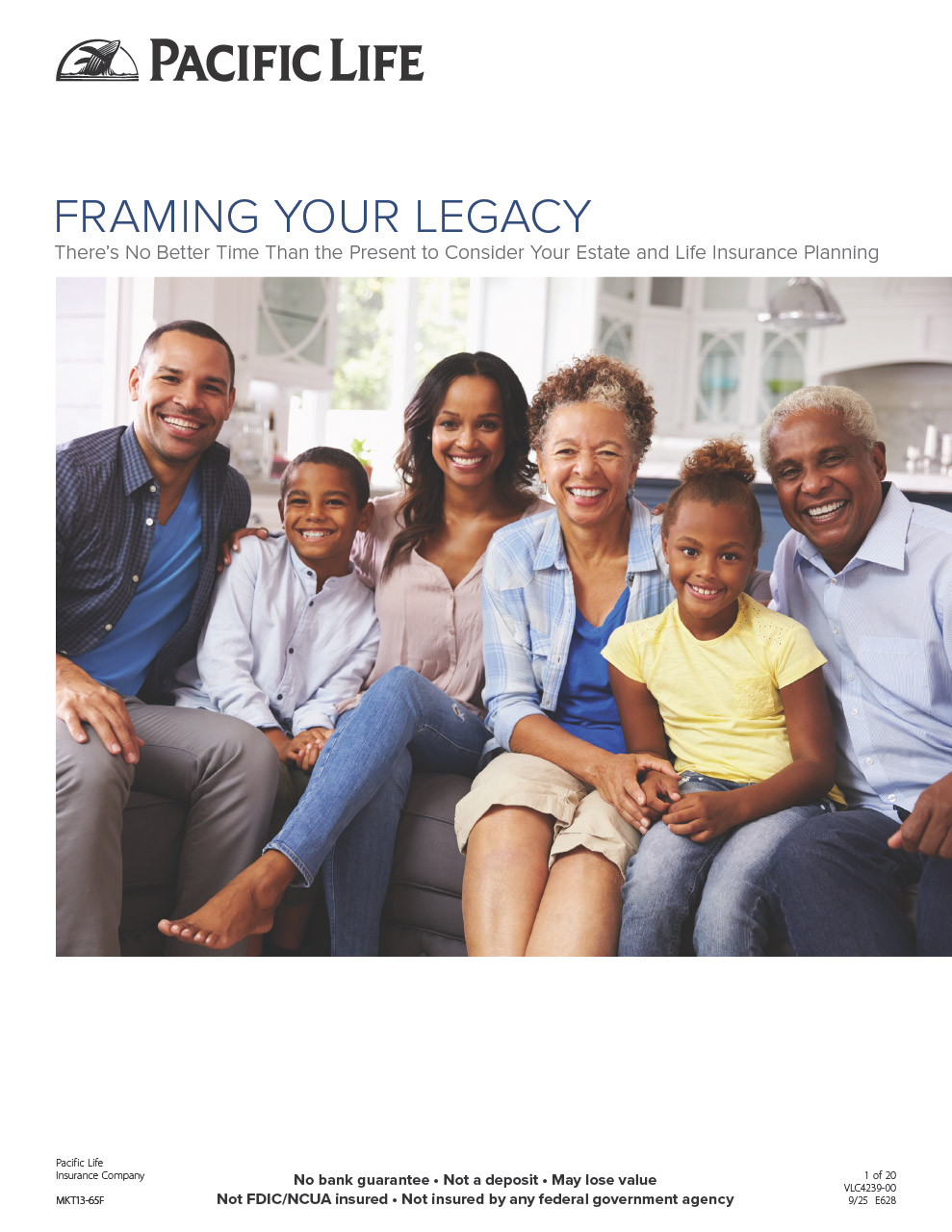

Utilize our Wealth Transfer Checklist and Framing Your Legacy brochure to help guide conversations with your clients and identify next steps.

2. Let Education Lead The Way

Tap into the experience of our Advanced Designs Unit (ADU) and stay on top of complex estate planning and taxation issues. Look to them for information on advanced strategies, including trusts, for enhancing wealth transfer.

3. Establish Relationships with Heirs and Advisors

Schedule meetings to get to know your clients’ advisors and stakeholders. They may become your future clients and collaborators in multigenerational wealth transfer.

4. Choose a Wealth Transfer Strategy

Help your clients select transfer strategies to reduce or eliminate unnecessary expenses, delays, probate or legal issues, taxes, or other challenges.

5. Consider Including Life Insurance

In addition to death benefit protection, life insurance can be a tax-advantaged and effective tool to help clients fulfill their final wishes and preserve their legacy. It can help offset potential estate taxes and accomplish other important financial goals.

6. Keep the Conversation Going

Make sure to conduct annual reviews with clients on their wealth transfer strategy or check-in whenever they experience major life events. Tax laws and assets can gain or lose value. We can help!

Take the Next Step

Your Pacific Life team can help you create a personalized wealth transfer plan for your clients.

Explore Popular Resources

The primary purpose of life insurance is death benefit protection.

Life insurance is subject to underwriting and approval of the application and will incur monthly policy charges. In general, additional premium is required to continue coverage of the policy. Policy may lapse if premium is insufficient to continue.

Pacific Life, its affiliates, their distributors, and respective representatives do not provide tax, accounting, or legal advice. Any taxpayer should seek advice based on the taxpayer’s particular circumstances from an independent tax advisor or attorney.

Insurance products and their guarantees, including optional benefits and any crediting rates, are backed by the financial strength and claims-paying ability of the issuing insurance company. Look to the strength of the insurance company with regard to such guarantees because these guarantees are not backed by the independent broker/dealers, insurance agencies, or their affiliates from which products are purchased. Neither these entities nor their representatives make any representation or assurance regrading the claims-paying ability of the issuing company.

1Source: "Cerulli Anticipates $84 Trillion in Wealth Transfer Through 2045," Cerulli Associates, January 20, 2022.

2"2023 Wills and Estate Planning Study", 2023 Wills and Estate Planning Study - Caring.com, January 2023, Caring.com.

3For federal income tax purposes, life insurance death benefits generally pay income tax-free to beneficiaries pursuant to IRC Sec. 101(a)(1). In certain situations, however, life insurance death benefits may be partially or wholly taxable. Situations include, but are not limited to: the transfer of a life insurance policy for valuable consideration unless the transfer qualifies for an exception under IRC Sec. 101(a)(2)(i.e. the transfer-for-value rule); arrangements that lack an insurable interest based on state law; and an employer-owned policy unless the policy qualifies for an exception under IRC Sec. 101(j).

Investment and Insurance Products: Not a Deposit • Not Insured by any Federal Government Agency • Not FDIC Insured • No Bank Guarantee • May Lose Value