Pacific Admiral ® VUL 2

Flexible Premium Variable Universal Life Insurance 1

Key Features

Beyond death benefit protection, Pacific Admiral VUL 2 offers flexible choices to support retirement, business, and estate planning needs.

Strong performance potential across ages and risk classes for death benefit protection, cash value growth potential, and no‑lapse guarantees

66 variable investment options, including low‑cost index funds, built for market‑driven growth potential. For downside protection, a choice from two indexed accounts³ with 0% guaranteed minimum interest crediting rates and one Fixed Account with a 1% guaranteed minimum interest crediting rate

Automatically includes Up to Age 90 No‑Lapse Guarantee Rider on eligible policies at no additional charge⁵ or up to lifetime no‑lapse guarantee via an optional rider with a monthly charge (investment option restrictions apply)⁴˒⁶

Three coverage types with a focus on long‑term accumulation potential,⁷˒⁸ early‑year cash surrender values with no surrender charges,⁷˒⁹ or something in‑between⁷

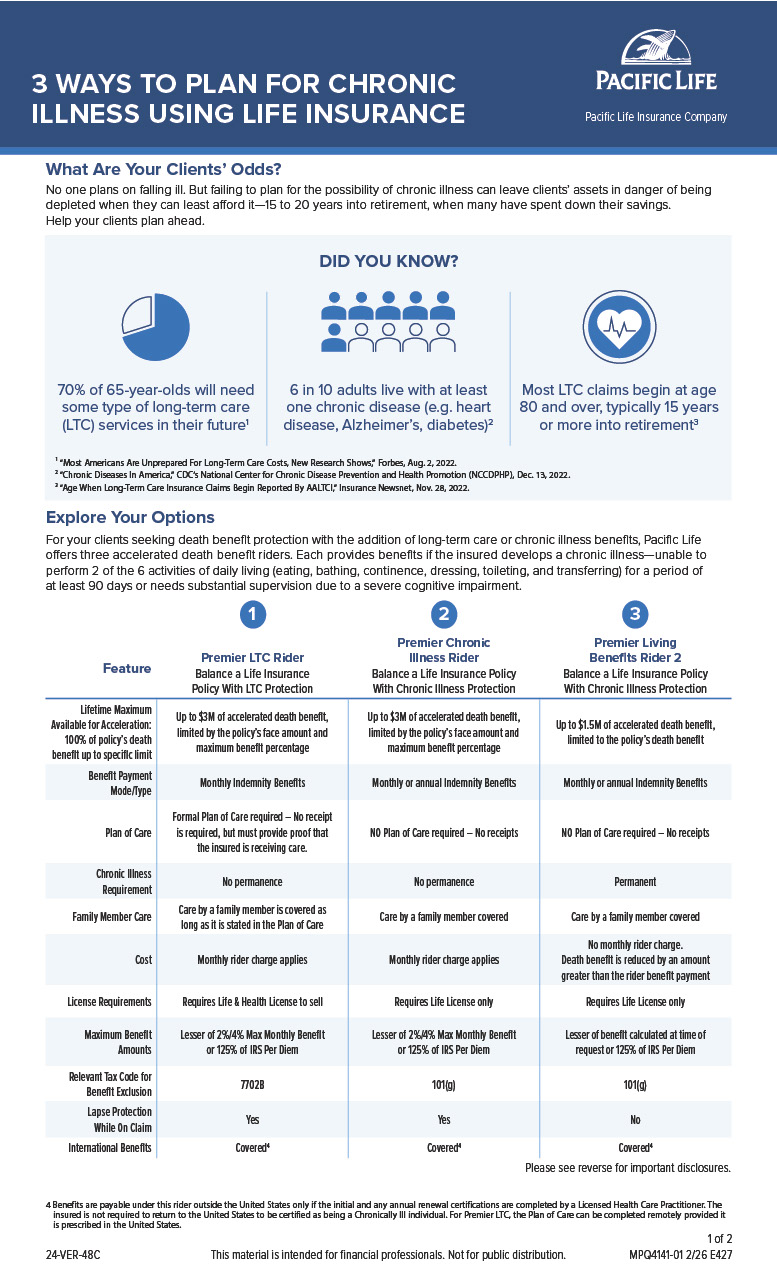

Choice between two optional chronic illness riders⁴˒¹⁰˒¹¹ or a long‑term care rider⁴˒¹²

Empower clients to achieve their accumulation goals.

Reach out to learn what Pacific Admiral VUL 2 could do for your clients.

Not all products or optional benefits are available in all states or firms, and features may vary by state and firm. Contact your firm or Pacific Life representative for availability.

1Pacific Admiral VUL 2 (Form series, P25VIUL, S25ADM2, varies based on state of policy issue).

2The issue ages for this product are 0-90.

3The indexed accounts do not directly participate in any index or the stock market.

4Riders may be subject to additional charges, availability, restrictions, and limitations. Clients should be shown policy illustrations with and without riders to help show the rider’s impact on the policy’s values.

5Up to Age 90 No-Lapse Guarantee Rider (Form series R22NLG, S22NLG, varies based on state of policy issue) is issued with all policies electing Death Benefit Option A or B with insured’s issue age 79 and under. Paying only the Up to Age 90 No-Lapse Premiums will guarantee the death benefit up to the insured’s attained age 90 but will not guarantee cash value accumulation. If your client discontinues paying the no-lapse guarantee premiums, the no-lapse feature will terminate before the guaranteed duration. If this occurs, additional premiums in an amount equal to the shortfall can be paid to bring the no-lapse feature back in force. If policy loans or withdrawals are taken, additional premiums may be required to keep the no-lapse feature in force. Additional premiums may be required to continue the policy beyond the guaranteed duration.

6The Flexible Duration No-Lapse Guarantee Rider (Form series R25FNL, S25FNL, varies based on state of policy issue), depending on how your client structures their policy, has a maximum duration up to the insured's lifetime, subject to certain limits. If your client’s net no-lapse guarantee value is zero, the no-lapse feature terminates. If the no-lapse feature terminates, additional premiums would be required to resume the no-lapse guarantee. If policy performance is such that your client’s policy is being maintained solely by the no-lapse guarantee, your client’s policy will not build cash value. For the rider’s guarantee to remain in place, the policyowner must not request an unscheduled increase in face amount and must remain 100% allocated among any of the Fixed Option, Indexed Options, and the other Allowable Investment Options specified in the prospectus.

7Each coverage type—including those offered through riders—incurs its own set of charges with unique features and benefits, subject to availability, restrictions, and limitations. When considering coverage types, clients should be shown policy illustrations with and without riders to help show the impact on the policy’s values.

8Available via Long-Term Performance Rider (Form series R25LTP, S25LTP2, varies based on state of policy issue).

9Available via SVER-3 Term Insurance Rider (Form series R18SV3, S18SV3, varies based on state of policy issue).

10Premier Chronic Illness Rider (Form series R22CHR, S21CHR, varies based on state of policy issue). Benefit payments reduce the policy’s death benefit and other values under the policy. If the entire death benefit is accelerated, the policy will terminate. Benefits paid by accelerating the policy’s death benefit are intended to qualify as death benefits under section 101(g) of the Internal Revenue Code and may be excludable from your income and may not be subject to federal taxation. However, federal, state, and/or local tax rules relating to the payment of accelerated death benefits are complex, will depend on your specific facts and circumstances, and benefits may or may not be taxable. In addition, these payments may affect eligibility for other benefits provided by federal, state, or local government including public assistance programs such as Medicaid. When benefits are received from multiple policies providing long-term care or chronic illness benefits for a given insured, including policies with different owners, all of those benefits must be aggregated to determine their taxability. Consequently, advice and guidance should be obtained from a personal tax advisor for more information. Pacific Life cannot determine whether the benefits are taxable. Currently not available in the state of California.

11Premier Living Benefits Rider 2 (Form series R18ADB, S18ADB, varies based on state of policy issue). Rider benefit payments will reduce policy values, including death benefit, cash surrender value, and policy debt, and may adversely affect the benefits under other riders. Benefits paid by accelerating the policy’s death benefit are intended to qualify as death benefits under section 101(g) of the Internal Revenue Code and may be excludable from your income and may not be subject to federal taxation. Tax treatment may depend on factors such as the amount of benefits, the amount of qualified expenses incurred, or if similar benefits are being received under other contracts. These amounts may also be in relation to certain IRS limitation (referred to as per diem limits). Tax laws relating to accelerated death benefits are complex. Receipt of accelerated death benefits may affect eligibility for public assistance such as Medicaid. When benefits are received from multiple policies providing chronic illness benefits for a given insured, including policies with different owners, all of those benefits must be aggregated to determine their taxability. Pacific Life cannot determine whether the benefits are taxable. If there are any questions concerning the tax implications of these riders, a qualified and independent legal and tax advisors should be consulted. The Premier Living Benefits Rider 2 comes standard with the policy if your client is eligible, but they can opt out by submitting a request.

12Premier LTC Rider (Form series R16LTC, R16LTCV SP, R16LTCV NLGI SP, varies based on state of policy issue). This is an accelerated death benefit rider for long-term care and is subject to eligibility and underwriting approval. The policy to which this rider is attached is subject to a medical exam, Medical Information Bureau (MIB), and prescription report; and may include obtaining records from your physician, a Personal History Interview, and a Cognitive Assessment. The amount and duration of the maximum LTC benefits and the rider charge will vary based on the benefit options elected at time of application and the use of policy benefits and features. The rider charge is included as part of the monthly deduction for the policy. Rates for long-term care coverage under this rider may increase over time, but not above those stated in the policy. This rider is intended to provide federally tax-qualified long-term care insurance as defined in IRC Section 7702B(b). When benefits are received from multiple policies providing long-term care or chronic illness benefits for a given insured, including policies with different owners, all of those benefits must be aggregated to determine their taxability. Pacific Life cannot determine whether the benefits are taxable. If there are any questions concerning the tax implications of this rider, qualified and independent legal and tax advisors should be consulted. Tax treatment may depend on factors such as the amount of benefits, the amount of qualified expenses incurred, or if similar benefits are being received under other contracts. Tax laws relating to accelerated death benefits are complex. Receipt of accelerated death benefits may affect eligibility for public assistance programs such as Medicaid. Clients are advised to consult with qualified and independent legal and tax advisors for more information. The PLTC benefits accelerate the policy’s death benefit and will reduce any proceeds payable upon the insured’s death or at time of surrender. Rider benefit payments will reduce policy values, including death benefit, cash surrender value, and policy debt, and may adversely affect the benefits under other riders. Policy charges for this rider and other riders are deducted from the policy’s accumulated value on a monthly basis. Policy lapse will only occur where the policy’s cash value less policy debt is not sufficient to cover monthly policy charges, unless a no-lapse guarantee is in effect. Prior to lapse, the policy provides 61 days to pay premium sufficient to keep the policy in force.

Clients should carefully consider a variable life insurance product’s risks, charges, limitations and expenses, as well as the risks, charges, expenses, and investment goals/objectives of the underlying investment options. This and other information about Pacific Life Insurance Company are provided in the applicable product and underlying funds prospectuses including summary prospectuses, if available. These prospectuses should be read carefully by clients before investing or sending money. Available by visiting pacificlife.com/Prospectuses and consider its information carefully before investing.

Variable insurance products are distributed by Pacific Select Distributors, LLC (member FINRA & SIPC), a subsidiary of Pacific Life Insurance Company and are available through licensed third-party broker-dealers.

Insurance products and their guarantees, including optional benefits, and any crediting rates, are backed by the financial strength and claims-paying ability of the issuing insurance company, but they do not protect the value of the variable investment options. Look to the strength of the insurance company with regard to such guarantees because these guarantees are not backed by the independent broker-dealers, insurance agencies, or their affiliates from which products are purchased. Neither these entities nor their representatives make any representation or assurance regarding the claims-paying ability of the issuing company.

Life insurance is subject to underwriting and approval of the application and will incur policy charges.

Investment and Insurance Products: Not a Deposit • Not Insured by any Federal Government Agency • Not FDIC Insured • No Bank Guarantee • May Lose Value